In 2022, China’s Sanitary Ceramics Production Is Expected To Be 230 Million Pieces. The Sanitary Ware Export Keeps Growing.

The following article is from China Building and Sanitary Ceramics Association Author in building ceramics association

China Building and Sanitary Ceramics Association – Promote the culture of China’s ceramic and sanitary industry, publicize the implementation of national industrial policies, advocate industry environmental protection and energy saving, promote industry design innovation, respond to industry demands, and build a platform for industry exchanges, interaction and cooperation, to promote the technical progress and healthy and orderly development of the industry to provide services!

2021 is the “Fourteenth Five-Year Plan” the opening year. For China’s building ceramics and sanitary ware industry, it is also the first year of low-carbon development, but also the ups and downs and the stormy year.

From the macro and policy side, the industry is subject to macro-control of real estate policy, energy consumption in many places, “double control” policy impact. The “carbon peak, carbon neutral” target was launched, energy consumption targets were tightened, and new construction and reconstruction projects were difficult.

From the market side, one, the “Evergrande incident” marked by the real estate enterprises “burst” phenomenon continues to appear, which brings a greater negative impact on the enterprise. Second, the second half of the weakening of domestic demand showed. Ceramic tile production has been slightly depressed. Supply and demand are both weak concentrated.

From the enterprise side, the supply shock has had a huge impact on the industry. Energy costs, raw material prices continue to climb, which obviously raised the cost of production. Business competition is becoming increasingly feverish, leading to a decline in the profitability of many enterprises.

Overall, in 2021, the overall operating situation of the industry as a whole remains stable and progressive. But there are also worries in the stability. The decline in market demand, the more obvious market differentiation, energy costs, fluctuations in raw material prices, energy consumption “double control” policy implementation, etc. increased the volatility of the economic operation of the building ceramics and sanitary ware industry.

Outlook for 2022, in the context of China’s sustained economic development, the industry’s development prospects are still promising. In 2022, China’s building ceramics and sanitary ware industry facing the macro-run environment is still expected to remain stable, but uncertainty still exists. Building ceramics and sanitary ware industry will be “carbon peak, carbon neutral” as the direction. They will comprehensively promote energy saving and comprehensive utilization, with technological innovation and brand building as the driving force, high-quality development as the focus, industrial restructuring, extending the industrial chain and “Internet +” application and promotion as the way. They focus on value-added services to promote the industry to green cycle low-carbon, innovation-driven and high-quality and efficient development and upgrading.

Overall industry-wide operation in 2021

In 2021, under the overlapping effects of the global spread of the Covid-9 epidemic, the continuous recovery of the global economy, the increase of domestic structural contradictions and the multi-point distribution of the epidemic, the promotion of the “double carbon” target, the continuous structural contradictions in the industry and the “mine-out” incidents of real estate enterprises, etc., the industry as a whole will be in a better position to meet the challenges and opportunities. Under the opportunities and challenges, the whole industry always adhered to the keynote of seeking progress in stability, overcame difficulties with resilience, calmly coped with the century-old changes and the epidemic of the century, and took new steps to build a new development pattern, achieving a steady start of the 14th Five-Year Plan. Real estate policy regulation led to the national real estate market demand contraction, and the overall weakening of the pulling effect of the ceramic tile application market. National sanitary ware production basically remained stable. Strong demand from foreign markets partially compensated for the decline in domestic market demand. In 2021, the epidemic was repeated. Against the background of a complex and volatile external environment, the foreign trade in architectural ceramics and sanitary ware products developed steadily. By the energy consumption of many places “double control” policy, production has slowed down. Coupled with energy prices, raw materials and other factors cost escalation led to the price of building ceramics and sanitary ware products increased significantly. In the fluctuating market situation, the overall performance of leading enterprises to deal with the market impact is good. In the new round of expansion, embracing capital and mergers and acquisitions accelerated, constantly seeking to expand production capacity and expand market share, and further strengthen the comprehensive strength. Cross-border competition, new business models and channel changes, new materials and new technologies accelerate industry reshuffling. The industry opens the journey of intelligent manufacturing, and production efficiency is significantly improved. In the context of double carbon, energy consumption, energy consumption indicators become an important factor affecting the production of ceramic industry. A new revolution in energy conservation and emission reduction marked by ceramic factories to invest in rooftop distributed photovoltaic projects is kicking off. The policy elimination further pushes the industry to transform and upgrade. The results achieved by the elimination of backward production capacity has been further consolidated, and the concentration of the industry has been further improved. Industrial structure is more optimized, innovative and personalized products increased significantly. The products such as ceramic rock slabs, outdoor ceramic thick tiles and eco-healthy new materials inject new vitality into the industry development. In the post-epidemic era, health, the market acceptance and popularity of intelligent sanitary products increased, young consumer groups gradually become the main body of social consumption, consumer upgrading, personalized demand for one-stop service to customize the bathroom is sought after by the market. The structure of the enterprise has a new change, showing the scale of the large brand enterprises and niche enterprises with special characteristics of synergistic development, complementary situation. Industry innovation capacity to further enhance. The level of domestic technology and equipment in the dry powder production process and equipment, remote digital ceramic (rock plate) grinding and polishing anti-fouling intelligent manufacturing system and process technology, multi-layer roller type electric heating lightweight microcrystalline stone production line, ceramic digital glaze key technology are in the overall improvement. Its international competitiveness has been further improved and the gap with foreign advanced level has been narrowed. The industry’s competition is also changing, from product iteration and channel change, to cross-border development, and then to the change of the track with the addition of capital. The boundaries of its market competition are expanding. The industry has changed benignly from the past crude development to the direction of standardization and high-quality development. But at the same time, the elimination of backward production capacity is not enough, R & D innovation capacity needs to be improved, and the ability to respond to market changes is weak and other bottlenecks that limit the healthy development of the industry still exist.

Sanitary products

This year, sanitary ware enterprises are relatively less affected by market changes than ceramic tile enterprises. The main reason is that, first of all, the overall demand for sanitary ware market continues to remain stable, and even a small increase. This is mainly because the international market has strong demand for Chinese sanitary ware products. Partly compensate for the impact of the decline in the domestic demand market. Along with the gradual recovery of the world economy from the impact of the Covid-19 epidemic, the foreign trade situation of Chinese sanitary ware enterprises is very good in 2021. On the other hand, it is also because the sanitary products market demand lags behind the objective law of ceramic tiles. In 2021, there will be varying degrees of growth in national sanitary ceramics and hardware sanitary ware production, main business income and profits. Resources are increasingly concentrated to the head of the enterprise, and the brand advantage is becoming more and more obvious. In the sanitary products market, international brands have always occupied a larger share of the domestic, especially in the high-end part of the market is more prominent. Since the Covid-19 epidemic, the national tide has been rising. The quality and efficiency of outstanding national brand companies have improved significantly. It has further expanded its market share, so the market also basically maintains a balanced supply and demand structure. Affected by the epidemic, consumers’ awareness of home health is rising, and the demand for healthy, intelligent and functional bathroom products has increased unprecedentedly. The sales of intelligent products such as intelligent toilets and intelligent bathroom cabinets are on the rise year by year, and their market penetration rate is also increasing year by year. To a certain extent, this has accelerated the development process of healthy and intelligent sanitary products. Full bathroom customization products and services have taken shape and show the potential for vigorous development. This is expected to become a new growth point of the bathroom market. The export volume and export value of sanitary ceramics and hardware sanitary products achieved double-digit growth at the same time. The growth curve continues to rise, to maintain the global bathroom market supply and demand balance provides a strong guarantee.

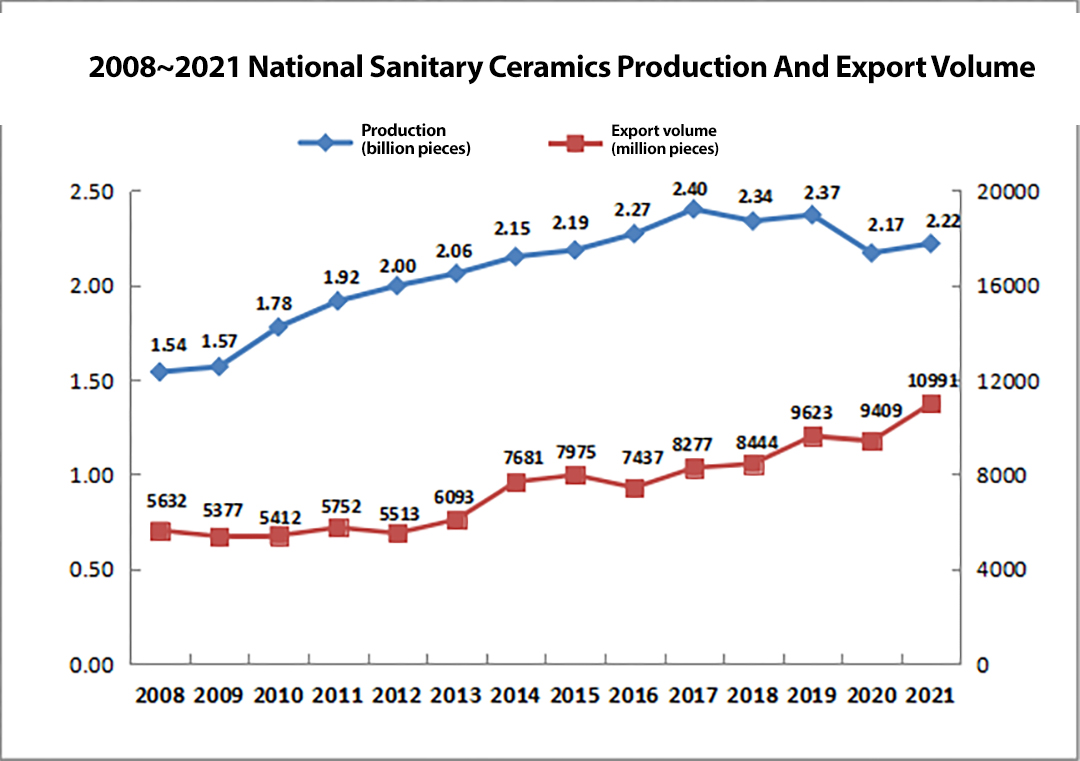

In 2021, the national scale of sanitary ceramics enterprises accounted for 363, an increase of 7. According to my survey to understand and statistics: the national production of sanitary ceramics above the scale is 223 million pieces, an increase of 2.5%. Sanitary ceramics in the main production areas, Guangdong, Hebei, Fujian, Hubei, Hunan production areas have different degrees of growth. The production area of Henan is affected by the double control, pulling the power to limit the impact of the larger, and production fell by more than 10%.

In 2021, China’s sanitary ceramics export volume and export value are creating a new record high. Among them, the export volume for the first time achieved on 100 million pieces of production, for 110 million pieces, an increase of 16.82% over 2020. Its export value reached 9.878 billion U.S. dollars, an increase of 12.13%. This is an average of $89.87 per piece, down 4.02% from the previous year. Sanitary ceramics exports have been growing since 2016, with the exception of a small dip in exports in 2020 due to the impact of the epidemic. Also due to the low base in 2020, overlaid with the worldwide growth in demand for sanitary ceramics and the lack of overseas production capacity, the growth rate increases and the growth curve steepens in 2021.

In 2021, the number of enterprise units above the size of the national plumbing, piping and building metal decorative materials industry was 1067. In January-December, the accumulated revenue of the main business of the plumbing, piping and building metal decorative materials industry above the scale was 159.550 billion yuan, an increase of 21.6% over the same period of the previous year. Its total profit accumulated 7.867 billion yuan, an increase of 15.96% over the same period last year. Sales profit margin was 4.93%, a decrease of 0.24% over the same period last year.

Hardware and sanitary products (plumbing and plumbing and architectural metal decorative materials) exports grew strongly. Export value and export volume of all types of products basically achieved double-digit growth. Total exports of hardware and sanitary products was $10.690 billion, an increase of 26.85%. This is partly due to the epidemic prompted foreign consumers to improve their personal health and hygiene concerns, on the other hand is due to the change in consumer behavior during the epidemic, once vacation, dining out and other aspects of spending turned to home improvement and other aspects to enhance the home environment and comfort. The export unit price of hardware and sanitary products, in addition to a small decline in the toilet seat cover, all show a certain degree of growth. On the one hand, the price increase is affected by the rise in domestic raw material prices and shipping costs. On the other hand, this is also the value-added of China’s sanitary ware export products to enhance, from the low-end gradually to high-end transformation results.

Industry-wide development of new dynamics

Accelerate the reshuffling speed of the building ceramics and sanitary ware industry in the “double carbon” background

2021 is the “carbon peak, carbon neutral” development of the first year. A series of new policies and regulations related to the building ceramics and sanitary ware industry have been released one after another from the central to local governments. They put forward new requirements for the production, new construction and reconstruction of the building ceramics and sanitary ware industry, mainly related to clean production, safe production, energy saving and reduction of consumption, ultra-low emissions and other aspects. With the introduction of the “double carbon” policy, governments at all levels have further strengthened the supervision of high energy consumption and high emissions industries. For serious violations of the law or fail to meet the latest requirements of production, they will face production shutdown and remediation, or even shut down and eliminated and other penalties. At the same time, since the year 2022, Guangdong, Hubei, Fujian, Shenyang and other places have more than 200 pottery enterprises have been the first to be included in the scope of carbon emissions management. It can be foreseen that the next, the construction pottery industry will certainly be fully included in carbon emission management and carbon trading.

Energy consumption, energy consumption indicators, carbon trading and a series of policies and regulations on the implementation of the land will become an important factor affecting the production of the pottery industry. And this has a profound and significant impact on the future development of the building ceramic industry. For the future of the ceramic industry, if companies want to develop and expand production capacity, then first must take into account the carrying capacity of resources and the environment. Even if there is supply and orders, it will not be able to produce if there are no energy consumption indicators or failure to meet energy consumption standards. Investment in new lines will become airborne. The transformation of old lines will also become difficult. And those enterprises whose energy consumption does not meet the standard will most likely be eliminated in the new round of energy regulation storm. If it is said that the environmental protection storm and coal to gas conversion during the “13th Five-Year Plan” is one of the important factors to eliminate the backward production capacity or nearly a quarter of the enterprises out of the industry, then during the “14th Five-Year Plan”, energy consumption targets and “carbon trading “will become an important grip for governments at all levels to regulate the layout and development of the industry. The tightening of energy consumption targets and the implementation of the carbon emissions trading market will accelerate the pace of high-quality development and elimination of backward production capacity in the building pottery industry. According to my data accounting, it shows that carbon dioxide emissions from the building and sanitary ceramics industry is about 140-200 million tons per year, accounting for about 1.5%-2% of the total national emissions. Among them, the building ceramics carbon emissions accounted for nearly 96% of the industry, therefore, all ceramic enterprises still have a long way to go.

Traditional products to accelerate the “materialization, parts, spatialization” transition

With the rise of assembly-type construction, consumer upgrading continues to promote the demand for improved housing gradually increased, accompanied by a large number of redecoration, renovation, local adjustment needs. Consumers have raised higher requirements for quality of life and living environment. Whole package, semi-package, and designer have become the mainstream channels. In particular, the whole installation, all-inclusive has become the mainstream consumption mode of decoration. Ceramic sanitary industry belongs to the field of all-inclusive. Extension of product lines and extension of the industrial chain to the “home” development is an important way for enterprises to become bigger and stronger. In the past, consumers are used to buying and using a single product. Now and in the future, the development trend is to use the entire space as a product. Traditional products are accelerating to “materialization, parts, space” transition. The “service-oriented” enterprises will become the mainstream enterprises in the market. With the changing age structure of the consumer group and the needs of young consumers, material supply one-stop solution has become more and more obvious demand.

Since the second half of last year, many leading ceramic companies have begun to integrate “tile, rock and green new materials” finished product delivery system. Focus from product delivery to finished product delivery, from the supply of materials to system services, strengthen the finished product delivery system in the field of interior industrialization, to achieve the development of a new ecology from materials to finished products customized. The traditional industry perception will be completely overturned. Companies that can not adapt to this transformation, if not better meet the needs of future consumers, will fall into passivity. This requires enterprises to constantly technological innovation, product innovation, business model innovation. Without innovation, enterprises will have no soul, no development momentum and lose their source of life.

Capital support to help the leading enterprises, and quickly improve the concentration of the industry

In 2021, during the domestic epidemic repeatedly continued throughout the year, under the severe challenges of the dual control of national energy consumption and energy-saving carbon reduction policy deep impact on the traditional production and operation mode of the ceramic sanitary industry, the ceramic industry entered a big wave of industry reshuffle stage. In the new round of expansion, leading enterprises accelerate the speed of embracing capital, comprehensive strength to further enhance the industry’s concentration continues to rise. Dongpeng, Mongnls, Diou home, etc. as the representative of these capital + strength backed by the pottery enterprises showed an unstoppable expansion trend. This all makes the industry realize: the rules of the game has been transferred from the past single market competition to the competition of the capital market track. The market and resources are increasingly tilted to the head brand enterprises. Enterprises can only run in the sky if they are listed. If companies do not go public, they can only run on the ground. What you see in the sky of 10,000 miles is different from what you see on the ground. They can only better help the rapid development of the enterprise if they are combined with the capital market. Therefore, from Tianan New Material and Eagle Group completed asset reorganization, to Marco Polo, New Pearl and a number of ceramic sanitary ware companies also started the listing process in 2021 or are in the queue to go public. This includes following the Dao’s listing, Zhongyang new material also began to dock the capital market, accepting tens of millions of dollars from Plum Blossom Venture Capital. This is proof that the tentacles of capital has been extended from the ceramic enterprises to supporting enterprises. These leading enterprises are hoping to use the power of capital. Through the strategic layout, scale expansion and rapid expansion of brand influence and capture market share, it is foreseeable that, with the support of capital, the future will form a small number of “total solution type” platform oligarchy. This will undoubtedly have a positive effect on the overall progress of the industry.

New products, new technologies, new models blur the “border” between industries

In recent years, as the trend of assembled buildings to “standardize” building components and “industrialize” construction methods has become more prominent, consumer iterations, aesthetic upgrades and consumer demand for a better quality of life continues to rise. In the power of the technology revolution and other multiple factors together, the traditional building ceramic sanitary ware industry has accelerated the cross-border deep integration with the pan-home decoration materials, home appliances, furniture and other industries. Consumer acceptance of new materials, new products, new design is also increasing, for example, the market demand for intelligent sanitary products has been further released. The market penetration rate of intelligent sanitary products is gradually increasing. The rock panel industry is still in its initial stage. As a “cross-border new species”, with the tile slate and slate tile, whether in the original traditional tile channel, or cross-border into the home furnishing, furniture, home appliances market, it will bring unlimited possibilities, as well as consumer awareness of home health in the rising. New eco-healthy materials preferred by the market, etc. are greatly for the industry to broaden the market boundary. The traditional building materials and home furnishing industry accelerates to “big home” integration. It is also due to the new products, new technologies, new models blurred the “border” between the industry, which makes the competition of the industry’s head enterprises has returned from the competition of the previous marketing model to the competition of R & D investment, manufacturing, product innovation capabilities. Who can produce better physical properties and visual effects and produce a higher replacement for traditional decorative materials, who can occupy the minds of consumers and win a larger market. Therefore, we want to take ceramics as a link, with the power of the scientific and technological revolution, to support the level of innovation technology to achieve breakthrough, disruptive innovation. We want to break the original boundaries, redefine the boundaries of the industry, and research and production of new materials and new products that are more in line with the needs of modern living environment. This is the new path of high-quality development of the industry, but also a new way out of the enterprise breakthrough.

Leading enterprises preemptively layout intelligent manufacturing, leading the transformation and upgrading of traditional manufacturing industry

As a labor-intensive traditional manufacturing industry, the construction of ceramic sanitary ware industry faces difficulties in recruiting workers, and labor costs have been significantly increased has been the bottleneck problem that restricts the development of the industry. Although the “Thirteenth Five-Year Plan” period, the ceramic tile enterprise per capita labor productivity increased by 50%. The sanitary ceramics enterprise per capita labor productivity increased by 30%, but still difficult to keep pace with the national economic development. This is far from meeting the needs of employees to improve the working environment. In the face of a new round of fierce competition and transformation and upgrading tide in the global manufacturing industry, especially the arrival of the post-epidemic era in 2020, it accelerated the intelligent production of building ceramic sanitary ware enterprises. A number of leading enterprises have taken the lead in promoting intelligent layout, building enterprises that integrate industrialization and informatization, improving production levels, operational efficiency, improving technology, innovating industrial models, providing new value for users, and seizing market opportunities.

According to the “Fourteenth Five-Year Plan”, the per capita labor productivity of the whole staff of ceramic (including rock slabs) enterprises should exceed 1.2 million yuan. The productivity of sanitary ceramics enterprises per capita labor exceeded 600,000 yuan, in the “Thirteenth Five-Year Plan” on the basis of this, and then raise 50%. Machine generation is the road to the development of architectural ceramics and sanitary ware industry. In a few years ago, a ceramic tile production line requires 200 to 300 workers, and now the most advanced domestic ceramic tile production line requires only 50 people. The kiln temperature, product testing and grading and many other aspects are also more intelligent control, in order to achieve greater efficiency, energy-saving role in reducing consumption. The latest domestic sanitary ceramics production line take advantage of the “5G + industrial Internet” application to empower the digital transformation of the sanitary industry, with more than 50% fewer workers than in the past. The labor conditions of employees have been greatly improved, and labor productivity has increased significantly. This has set a benchmark for the transformation of raw industry manufacturing. In recent years, the industry has made great progress in digitalization and intelligence, further reducing the gap with the advanced foreign level.

2022 Outlook and Prognosis

2022 is an important year for China to embark on a new journey to build a comprehensive socialist modernization country and march towards the second century goal. In the face of the current intricate changes in the political and economic situation at home and abroad, the country has clearly and repeatedly stressed the “stable growth” tone, so “stable word in the forefront, steady progress” will become the main line of policy in 2022. In the new year, on the one hand, China’s sanitary ware industry should work together to overcome the difficulties and obstacles. At the same time we have to be based on the new development stage. We should also take “carbon peak, carbon neutral” as the direction, fully implement the continuous green low-carbon transformation, accelerate the adjustment of energy structure, and promote energy saving and comprehensive utilization. We should continue to take technological innovation and brand building as the driving force, focus on high-quality development, industrial restructuring, extending the industrial chain and “Internet +” application and promotion as a way to focus on value-added services, further promote the optimization and upgrading of industrial structure, and promote the industry to green cycle low-carbon, innovation-driven and high-quality and efficient development Upgrade. Although it is a long way to go, China has the world’s largest demand market and the Chinese economy is extremely resilient. In the context of China’s sustained economic development, the industry’s development prospects are still promising. But not all companies will survive. In the “double carbon” background, we will further accelerate the speed of bathroom industry reshuffle. The next few years, this market will be the survival of the fittest, and the competitive environment will be more “cruel”.

In 2022, China’s investment may show a rise in infrastructure investment and a low growth in real estate investment. Policy-driven investment will become the key to stable growth. In the context of “housing and housing without speculation” and the continued steady implementation of the long-term mechanism of real estate, real estate investment around the world may be based on the actual situation of the local real estate market to take more “city-specific” policies to promote the stability of real estate investment. In 2022, China’s sanitary ware industry is still expected to maintain a stable macro-run environment, but uncertainty still exists. It is expected that in 2022, the production of sanitary ceramics will continue to maintain in the range of 230 million pieces of operation. In international trade, with the overall improvement of the international epidemic situation, in 2022, China’s sanitary products exports will continue to maintain growth, the annual export amount is expected to exceed 30 billion U.S. dollars, which again set a new high.

WeChat

Scan the QR Code with WeChat